ARMA Model — System Identification Walkthrough

This notebook demonstrates the four-step system identification process for a univariate time series using the ARMA model class.

Step |

Task |

Tool |

|---|---|---|

1 |

Choose a model class |

Domain knowledge |

2 |

Select model order |

|

3 |

Estimate parameters |

|

4 |

Validate the model |

|

Dataset: Box-Jenkins Series A — Chemical Concentration (197 observations)

The ARMA(\(n_d\), \(n_c\)) model is

where

and

The noise is modeled by the transfer function \(H(q) = C(q)/D(q)\).

[2]:

import numpy as np

import matplotlib.pyplot as plt

import sys

import os

import pandas as pd

# Add TimeSeries root directory to path

current_dir = os.getcwd()

timeseries_root = os.path.abspath(os.path.join(current_dir, '..', '..', '..'))

if timeseries_root not in sys.path:

sys.path.insert(0, timeseries_root)

from TimeSeriesSRC.Model.model import pmodel

from TimeSeriesSRC.Model.estimate import estimate

from TimeSeriesSRC.Model.selpmod import func_selpmod as selpmod

from TimeSeriesSRC.basefunctions.uniAnal import func_uniAnal as uniAnal

from TimeSeriesSRC.basefunctions.uniChi import func_uniChi as uniChi

from TimeSeriesSRC.basefunctions.partoacf import func_partoacf_pmod as partoacf_pmod

from TimeSeriesSRC.Model.pmodmse import func_pmodmse as pmodmse

from TimeSeriesSRC.Model.pmoddisp import func_pmoddisp as pmoddisp

from TimeSeriesSRC.Model.pmoddisp import func_pmodpzplot as pmodpzplot

np.random.seed(42)

print('Setup complete.')

Setup complete.

Series A — Chemical Concentration

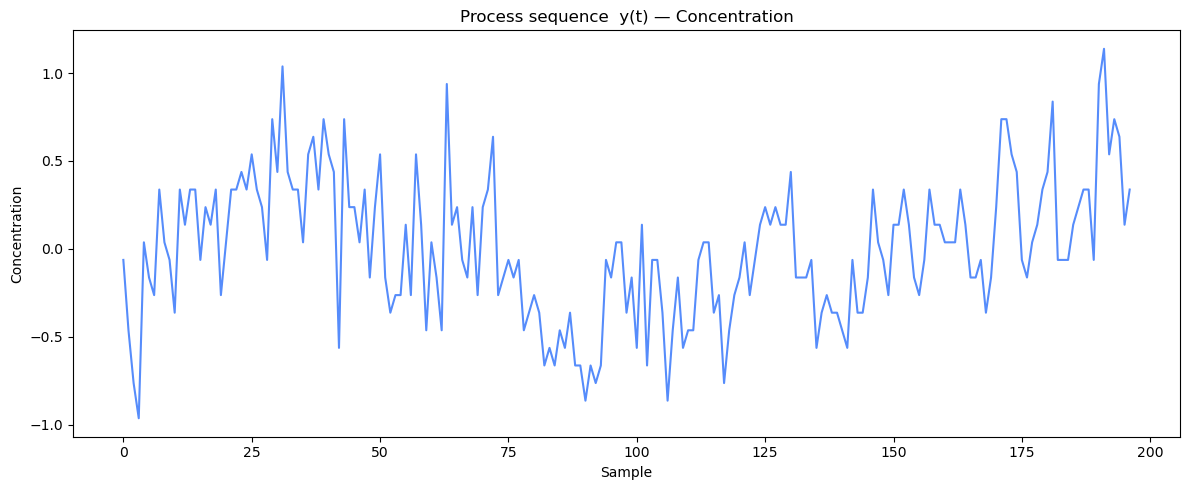

Box-Jenkins Series A is a univariate time series of 197 concentration measurements from a chemical process. There is no observed external input, making the ARMA class the natural starting point. The series mean is removed before modeling.

[3]:

data_path = os.path.join(timeseries_root, 'TimeSeriesSRC', 'TestData', 'Series_A_Chemical_Concentration.csv')

df = pd.read_csv(data_path)

y = np.array(df['Concentration'])

Step 1 — Choose a Model Class

With no external input, the general prediction model \(y(t) = G(q)u(t) + H(q)e(t)\) reduces to a pure noise model:

This is the ARMA(:math:`n_d`, :math:`n_c`) model, where \(D(q)\) is the autoregressive polynomial of order \(n_d\) and \(C(q)\) is the moving average polynomial of order \(n_c\). The orders are determined in Step 2.

[3]:

y = y - np.mean(y)

N = y.size

print(f'Loaded chemical process data: N={N} samples')

print(f'y: mean={y.mean():.2e}, std={y.std():.3f}')

fig, ax = plt.subplots(1, 1, figsize=(12, 5))

ax.plot(y)

ax.set_title('Process sequence y(t) — Concentration')

ax.set_xlabel('t')

ax.set_ylabel('Concentration')

ax.set_xlabel('Sample')

plt.tight_layout()

plt.show()

Loaded chemical process data: N=197 samples

y: mean=-2.74e-15, std=0.398

Step 2 — Select Model Order

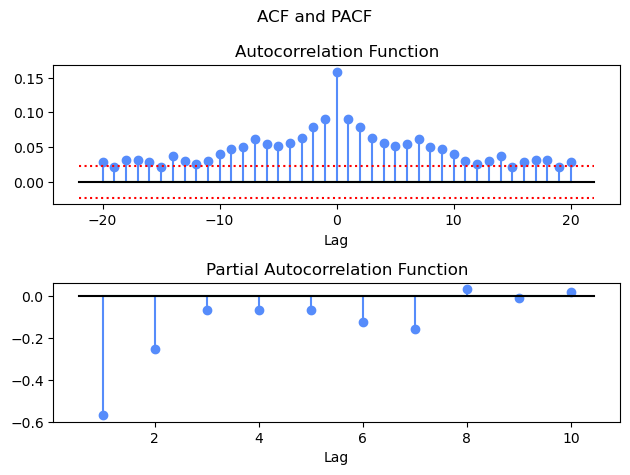

uniAnal computes the ACF, PACF, and Generalized Partial Autocorrelation (GPAC) of the series.

ACF — exponential or oscillatory decay suggests AR behaviour; a sharp cutoff at lag \(n_c\) suggests a pure MA model.

PACF — cuts off sharply after lag \(n_d\) for a pure AR model; decays slowly for a pure MA model.

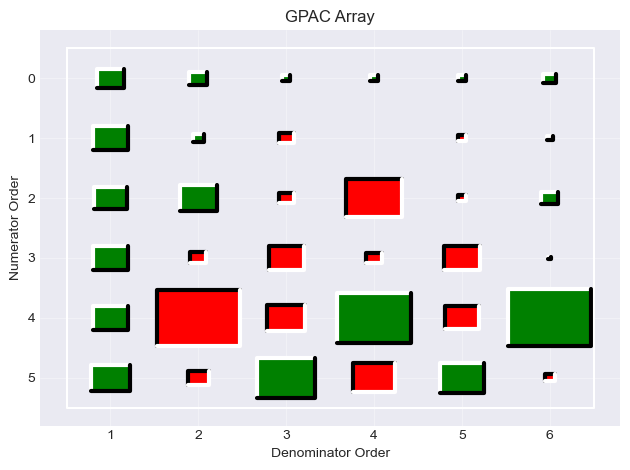

GPAC — the primary tool for ARMA order identification. A column of approximately constant (near-zero) entries identifies the AR order \(n_d\); the row at which the constant pattern begins identifies the MA order \(n_c\).

[4]:

acf, pacf, gpac = uniAnal(y, na=20, nump=10, nrg=6, ncg=6)

GPAC Interpretation

In the GPAC table, look for a column that becomes approximately constant (values near zero from some row onward):

The column index is the candidate AR order \(n_d\).

The row where the constant pattern begins is the candidate MA order \(n_c\).

For Series A, column 1 of the GPAC becomes approximately constant starting at row 1, indicating an ARMA(1, 1) model (\(n_d = 1\), \(n_c = 1\)).

Step 3 — Estimate Parameters

We fit an ARMA(1, 1) model — the structure indicated by the GPAC — using estimate, which minimises the sum of squared one-step prediction errors via the Levenberg–Marquardt algorithm.

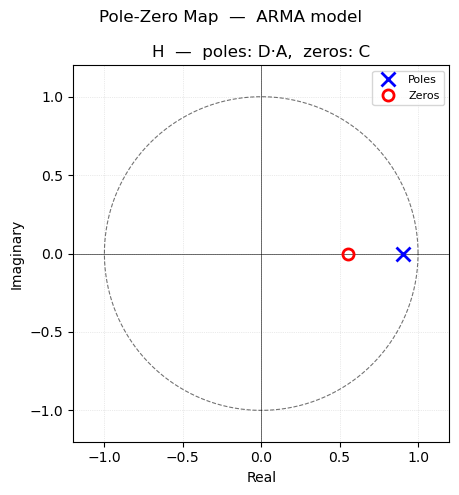

pmoddisp prints the estimated parameters with ±2σ confidence intervals and a confidence-interval plot. pmodpzplot shows the pole-zero map for the noise transfer function \(H(q) = C(q)/D(q)\), confirming stability and invertibility.

[5]:

pmod = pmodel('arma', nc=[1], nd=[1], diff=[0], per=[])

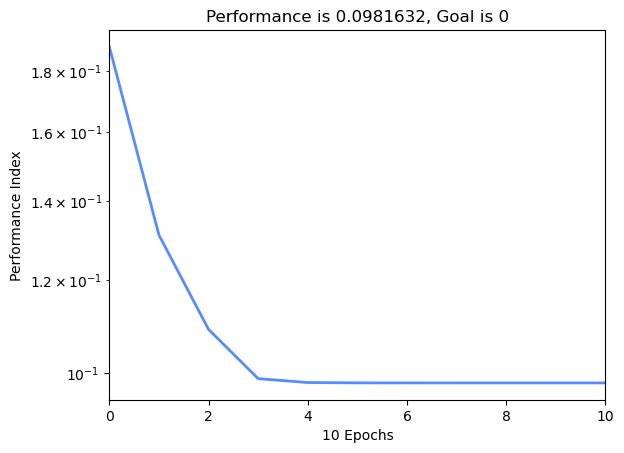

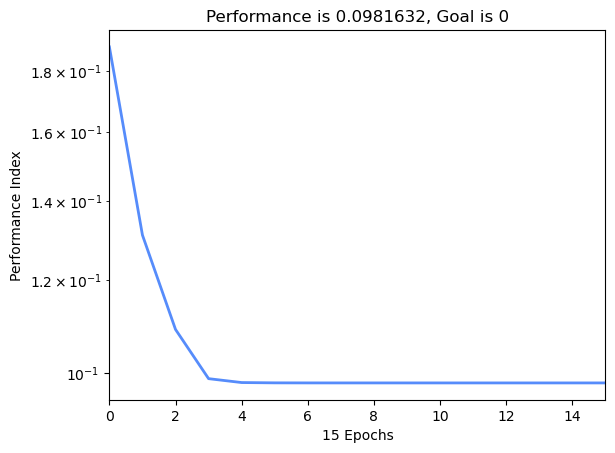

pmod, trec, stat = estimate(pmod, y)

Epoch 0/100 Time 0.0007948875427246094 PMODMSE 0.18876863441748454/0 Gradient 34.47996692994865/0.0001 mu 0.001/10000000000.0

Epoch 10/100 Time 0.1499190330505371 PMODMSE 0.09816324220471359/0 Gradient 0.0028234427030654425/0.0001 mu 1.0000000000000006e-10/10000000000.0

6.114089507982792e-05 0.0001

Epoch 15/100 Time 0.22534489631652832 PMODMSE 0.09816323622692254/0 Gradient 6.114089507982792e-05/0.0001 mu 1.0000000000000009e-15/10000000000.0

ESTIMLM, Minimum gradient reached, performance goal was not met.

[6]:

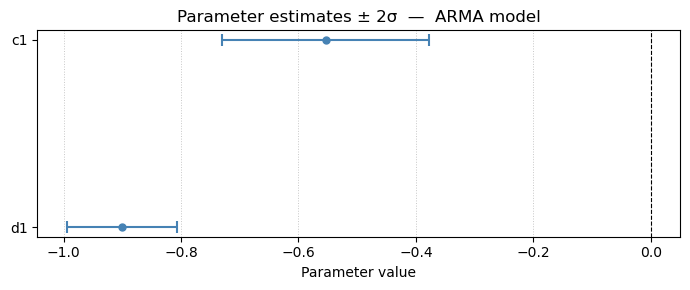

pmoddisp(pmod, stat)

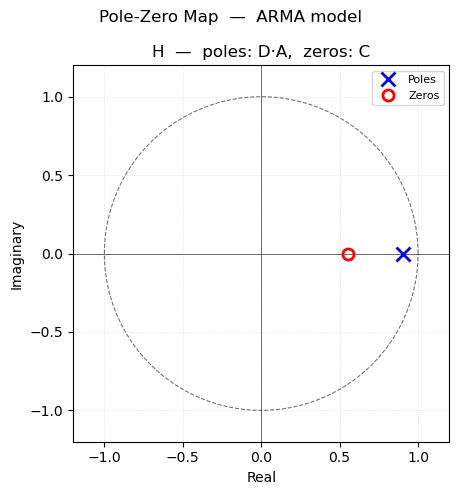

pmodpzplot(pmod)

plt.show()

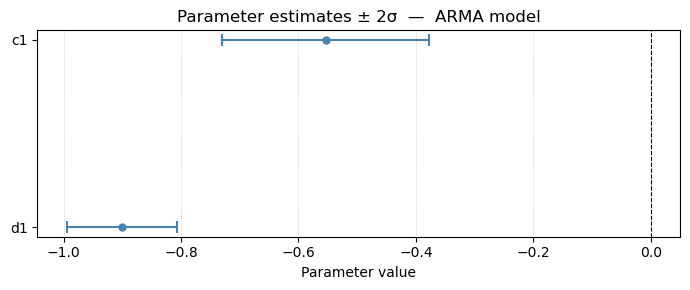

Parameter estimates — ARMA model

--------------------------------

Param Value ±2σ 95% CI

----------------------------------------

c1 -0.5536 0.1762 ( -0.7297, -0.3774)

d1 -0.9010 0.0936 ( -0.9946, -0.8073)

Residual std σ = 0.313310

Residual var σ² = 0.098163

Step 4 — Validate the Model

A well-fitted ARMA model should leave white residuals — uncorrelated errors with no remaining structure. We check this in three ways:

Theoretical ACF —

partoacf_pmodcomputes the theoretical autocovariance function of the fitted model using the Yule-Walker method. Overlaying it on the experimental ACF from Step 2 confirms that the model captures the correlation structure of the data.Residual ACF — plot the ACF, PACF, and GPAC of the residuals with

uniAnal. All values should fall within the 95% confidence bounds (dashed lines).Statistical test —

uniChiperforms the portmanteau chi-square test on the residuals. The null hypothesis is that the residuals are white noise; a p-value > 0.05 indicates an adequate model.

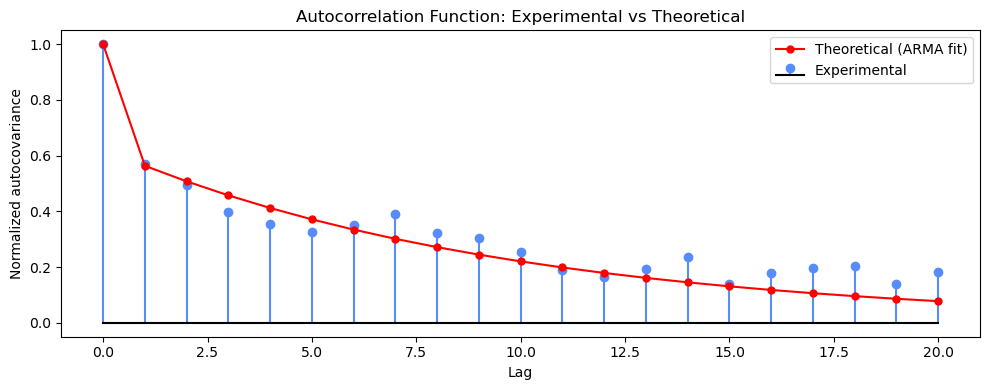

Check 1 — Theoretical vs Experimental ACF

partoacf_pmod uses the Yule-Walker equations to compute the exact autocovariance function implied by the fitted ARMA polynomials and the noise variance. Close agreement with the experimental ACF from Step 2 confirms that the model has captured the dominant correlation structure.

[7]:

# Noise variance estimate from one-step prediction errors

var_e, _ = pmodmse(pmod, y)

# Theoretical autocovariance function from the fitted ARMA(1,1) model

lagmax = 21

acf_theory, _, _ = partoacf_pmod(pmod, var_e, lagmax)

# Experimental ACF from Step 2: uniAnal returned acf of shape (1, 2*na+1)

# with na=20, so index 20 is lag 0; take the positive-lag half

acf_exp = acf.squeeze()[20:20 + lagmax]

# Normalize both to lag-0 = 1 for a shape comparison

acf_theory_norm = acf_theory / acf_theory[0]

acf_exp_norm = acf_exp / acf_exp[0]

lags = np.arange(lagmax)

fig, ax = plt.subplots(figsize=(10, 4))

ax.stem(lags, acf_exp_norm, linefmt='C0-', markerfmt='C0o', basefmt='k-', label='Experimental')

ax.plot(lags, acf_theory_norm, 'r-o', markersize=5, linewidth=1.5, label='Theoretical (ARMA fit)')

ax.set_title('Autocorrelation Function: Experimental vs Theoretical')

ax.set_xlabel('Lag')

ax.set_ylabel('Normalized autocovariance')

ax.legend()

plt.tight_layout()

plt.show()

[ ]:

e = y - pmod.predict(y)

print(f'Residual std: {e.std():.4f}')

acf_e, pacf_e, gpac_e = uniAnal(e, na=20, nump=10, nrg=6, ncg=6)

[8]:

#uniChi(pmod, y)

passed, q_arma, n_arma, pval = uniChi(pmod, y)

print(f'\nChi-square test on u residuals: Q={q_arma:.2f}, df={n_arma}, pass={bool(passed)}, pval={pval:.3f}')

print('(pass=True means residuals are consistent with white noise at 95% confidence)')

pval: 0.1040045634909047

alpha: 0.05

pr: 0.8959954365090953

q: 25.82270352305808

Chi-square test on u residuals: Q=25.82, df=18, pass=True, pval=0.104

(pass=True means residuals are consistent with white noise at 95% confidence)

Conclusion

The residual ACF is within the 95% confidence bounds (approximating an impulse function), the first row of the GPAC is approximately zero (indicating white noise) and the chi-square test is passed (p-value > 0.05), therefore the ARMA(1, 1) model is validated. .

The fitted parameter table from pmoddisp shows the estimated values with ±2σ confidence intervals, and none of the confidence intervals includes zero, which would indicate that a parameter could be removed. The pole-zero map from pmodpzplot confirms whether the AR and MA polynomials are stable and invertible — all poles and zeros should lie outside the unit circle. Also, there is no approximate pole/zero cancellation, which would indicate that the model orders could be reduced.

If the residuals show remaining structure, return to Step 2 and explore higher-order structures, or use selpmod for an automated grid search over ARMA orders.

Automated Model Selection with selpmod

selpmod performs a grid search over a set of candidate ARMA structures, estimating each one and ranking by AIC and BIC. We search over \(n_d \in \{1, 2, 3\}\) and \(n_c \in \{0, 1, 2, 3\}\) — 12 combinations — to verify that the ARMA(1, 1) structure identified in Step 2 is indeed optimal.

[9]:

arma_spec = {

'models': [{

'type': 'arma',

'nc': [0, 1, 2, 3],

'nd': [1, 2, 3],

'diff': [0]

}]

}

result = selpmod(arma_spec, y)

aicmod = result['arma']['aicmod']

bicmod = result['arma']['bicmod']

aicstat = result['arma']['aicstat']

bicstat = result['arma']['bicstat']

Selecting the best ARMA prediction model

arma: Combination 1 out of 12 total [nc=0, nd=1]. aic = -2.2262, bic = -2.2096

arma: Combination 2 out of 12 total [nc=0, nd=2]. aic = -2.2818, bic = -2.2485

arma: Combination 3 out of 12 total [nc=0, nd=3]. aic = -2.2771, bic = -2.2271

arma: Combination 4 out of 12 total [nc=1, nd=1]. aic = -2.3008, bic = -2.2675

arma: Combination 5 out of 12 total [nc=1, nd=2]. aic = -2.3013, bic = -2.2513

arma: Combination 6 out of 12 total [nc=1, nd=3]. aic = -2.2966, bic = -2.2299

arma: Combination 7 out of 12 total [nc=2, nd=1]. aic = -2.2979, bic = -2.2479

arma: Combination 8 out of 12 total [nc=2, nd=2]. aic = -2.2818, bic = -2.2151

arma: Combination 9 out of 12 total [nc=2, nd=3]. aic = -2.2846, bic = -2.2013

arma: Combination 10 out of 12 total [nc=3, nd=1]. aic = -2.2983, bic = -2.2317

arma: Combination 11 out of 12 total [nc=3, nd=2]. aic = -2.2809, bic = -2.1975

arma: Combination 12 out of 12 total [nc=3, nd=3]. aic = -2.3180, bic = -2.2180

[10]:

print(f'Best AIC model: ARMA(nd={int(aicmod.nd[0])}, nc={int(aicmod.nc[0])})')

print(f'Best BIC model: ARMA(nd={int(bicmod.nd[0])}, nc={int(bicmod.nc[0])})\n')

print('=== Best AIC model ===')

pmoddisp(aicmod, aicstat)

pmodpzplot(aicmod)

plt.show()

print('=== Best BIC model ===')

pmoddisp(bicmod, bicstat)

pmodpzplot(bicmod)

plt.show()

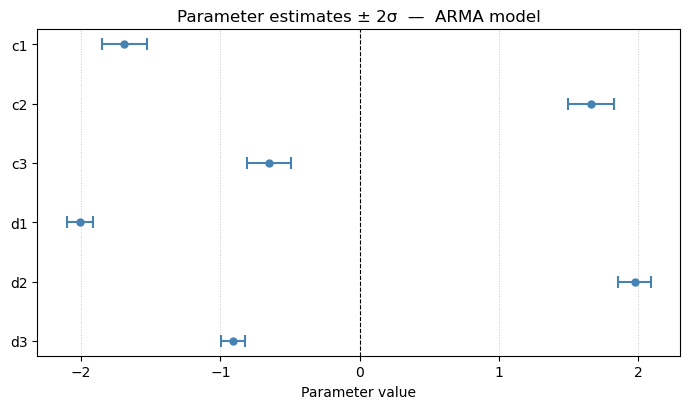

Best AIC model: ARMA(nd=3, nc=3)

Best BIC model: ARMA(nd=1, nc=1)

=== Best AIC model ===

Parameter estimates — ARMA model

--------------------------------

Param Value ±2σ 95% CI

----------------------------------------

c1 -1.6897 0.1603 ( -1.8500, -1.5294)

c2 1.6609 0.1663 ( 1.4946, 1.8271)

c3 -0.6489 0.1576 ( -0.8065, -0.4912)

d1 -2.0100 0.0935 ( -2.1035, -1.9165)

d2 1.9745 0.1165 ( 1.8580, 2.0910)

d3 -0.9062 0.0861 ( -0.9923, -0.8202)

Residual std σ = 0.304386

Residual var σ² = 0.092651

=== Best BIC model ===

Parameter estimates — ARMA model

--------------------------------

Param Value ±2σ 95% CI

----------------------------------------

c1 -0.5536 0.1762 ( -0.7297, -0.3774)

d1 -0.9010 0.0936 ( -0.9946, -0.8073)

Residual std σ = 0.313310

Residual var σ² = 0.098163

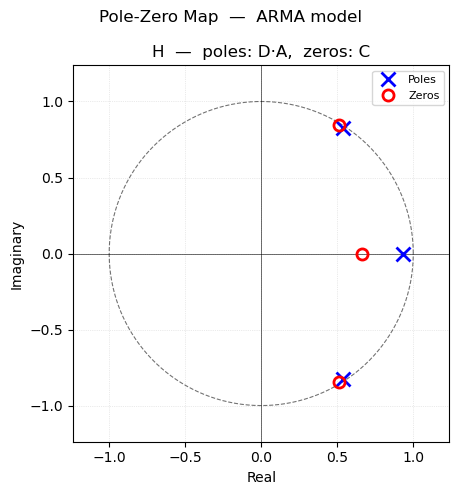

Notice that the best AIC model increased nc and nd by 2. However, when we look at the pole / zero plot, we see that there are pole / zero cancellations. After the cancellation, we revert back to the original model. The best BIC model is the same as the original model we selected from the preliminary analysis.